Economic Foundations |

|

Learning Resources

Supply/Demand Game

Supply and Demand Explained

Supply and Demand in Indiana Jones

Efficiency and Market Failure

GDP, Recession, and Fiscal Policy

Supply and Demand Explained

Supply and Demand in Indiana Jones

Efficiency and Market Failure

GDP, Recession, and Fiscal Policy

Topic Review

1. FUNDAMENTALS

A. NEEDS/WANTS

A need is something that one must have to survive (like food, water, or housing) whereas a want is something that is desired but not required (like jewelry)

B. GOOD/SERVICE

A good is something for sale that is physical and can be touched (like a soda) whereas a service is something that is done for someone (like lawn mowing)

C. SCARCITY

This is the basic economic problem: not enough goods and services to satisfy all needs and wants.

D. OPPORTUNITY COST & TRADE-OFFS

Opportunity cost is defined as the value of the next best alternative choice that was not made. Due to scarcity, we all have to make trade offs.

2. BASIC ECONOMIC QUESTIONS

What are the questions that all societies must answer?

A. WHAT TO PRODUCE?

B. HOW TO PRODUCE?

C. FOR WHOM TO PRODUCE?

3. ECONOMIC SYSTEMS

How to different societies answer the basic economic questions?

A. TRADITIONAL

The economy runs as it always has, with traditional roles being filled by men and women.

B. COMMAND (COMMUNIST/SOCIALIST)

The government or central authority decides how to answer the basic economic questions.

C. CAPITALIST

The marketplace decides the answers to the basic economic questions.

I. TRAITS OF THE FREE MARKET SYSTEM

1. PRIVATE PROPERTY

2. PROFIT MOTIVE

3. PRIVATE ENTERPRISE

4. COMPETITION

5. FREEDOM OF CHOICE

II. VARIATIONS

1. MONOPOLY

One company is the only supplier in an industry, so it can set availability and prices as it wants.

2. PURE/PERFECT COMPETITION

There are many suppliers competing for customers, theoretically reducing prices.

3. MONOPOLISTIC COMPETITION

A small number of companies compete for customers.

4. MIXED

Some combination of the above exists. This is the system we have in the U.S.

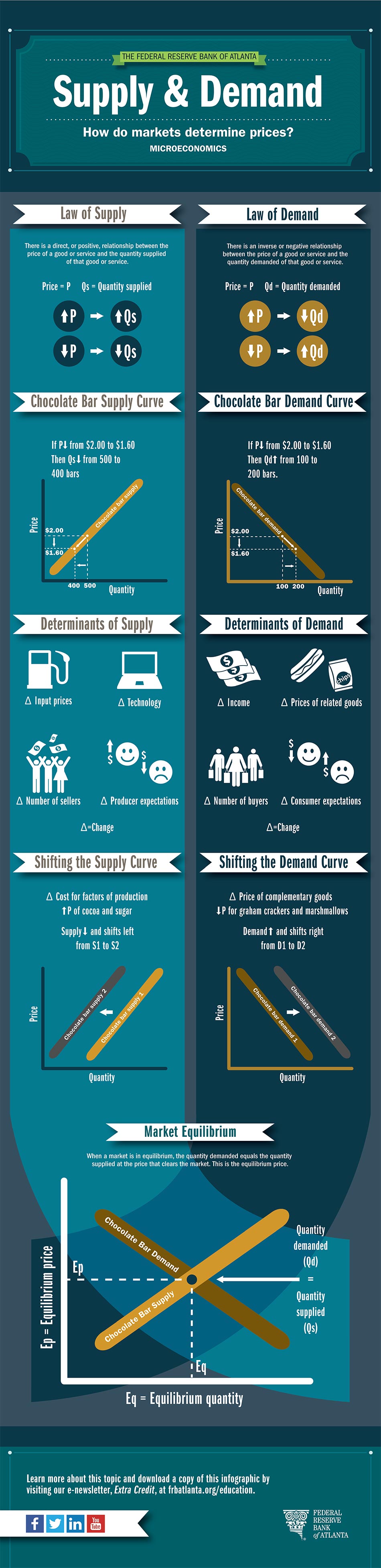

4. SUPPLY & DEMAND

Supply is the number of units producers are willing and able to sell. Demand is the number of units consumers are

willing and able to buy. The point where supply meets demand is called the equilibrium price.

CHANGES IN DEMAND OR SUPPLY WILL AFFECT PRICES

A. If demand is constant and supply goes up, prices will fall.

B. If demand is constant and supply goes down, prices will rise.

C. If supply is constant and demand goes up, prices will rise.

D. If supply is constant and demand goes down, prices will fall.

5. BUSINESS CYCLE

An economy goes through natural cycles of expansion and contraction.

A. PROSPERITY

Times are good. Unemployment is low. Consumer spending is relatively high.

B. RECESSION

The economy is slowing down. Unemployment is increasing. Consumer spending is slowing.

C. DEPRESSION

The economy is weak. Unemployment is high. Wages are low. Consumer confidence is low. There is reduced

business activity.

D. RECOVERY

Business activity is picking up. Unemployment is going down. Wages are increasing. Consumers increase

their buying.

6. INFLATION & DEFLATION

Inflation is when the cost of items increase over time, thus decreasing the value of each dollar earned. Deflation is when the cost of items decrease over time, thus increasing the value of each dollar earned.

7. CIRCULAR FLOW

This is a diagram to illustrate how money circulates in our economy.

A. PLAYERS

I. HOUSEHOLDS/PEOPLE

II. BUSINESSES/ENTREPRENEURS

B. MARKETS

I. FACTOR MARKET

1. FACTORS OF PRODUCTION: NATURAL RESOURCES, LABOR, CAPITAL, & ENTREPRENEURSHIP

Natural resources are things like mineral ore, forests, water, or corn. Labor refers to the workforce.

Capital is investment in businesses through the buying of stock. Entrepreneurship is the

development of business ventures.

2. INCOME: WAGES, RENTS, INTERESTS, PROFIT

II. PRODUCT MARKET

1. FINISHED GOODS & SERVICES

2. PAYMENT FOR GOODS & SERVICES

The circular flow diagram can also be expanded to include the banking and government players.

8. IMPORTANT ECONOMIC INDICATORS

A. CONSUMER PRICE INDEX

This measures the cost to consumers of a hypothetical "basket of goods".

B. GROSS NATIONAL PRODUCT (GNP)

This represents the total value of all goods and services produced by a country.

C. UNEMPLOYMENT RATE

This generally represents the percentage of people who are both able and looking to work but cannot find a

job.

D. INFLATION RATE

This is the yearly rate of in the cost of things.

E. HOUSING STARTS

A good measure of how the economy is doing is the number of new houses constructed. This is because it

represents new and large investment, which is a good

indicator of both business activity and consumer confidence in future economic activity.

A. NEEDS/WANTS

A need is something that one must have to survive (like food, water, or housing) whereas a want is something that is desired but not required (like jewelry)

B. GOOD/SERVICE

A good is something for sale that is physical and can be touched (like a soda) whereas a service is something that is done for someone (like lawn mowing)

C. SCARCITY

This is the basic economic problem: not enough goods and services to satisfy all needs and wants.

D. OPPORTUNITY COST & TRADE-OFFS

Opportunity cost is defined as the value of the next best alternative choice that was not made. Due to scarcity, we all have to make trade offs.

2. BASIC ECONOMIC QUESTIONS

What are the questions that all societies must answer?

A. WHAT TO PRODUCE?

B. HOW TO PRODUCE?

C. FOR WHOM TO PRODUCE?

3. ECONOMIC SYSTEMS

How to different societies answer the basic economic questions?

A. TRADITIONAL

The economy runs as it always has, with traditional roles being filled by men and women.

B. COMMAND (COMMUNIST/SOCIALIST)

The government or central authority decides how to answer the basic economic questions.

C. CAPITALIST

The marketplace decides the answers to the basic economic questions.

I. TRAITS OF THE FREE MARKET SYSTEM

1. PRIVATE PROPERTY

2. PROFIT MOTIVE

3. PRIVATE ENTERPRISE

4. COMPETITION

5. FREEDOM OF CHOICE

II. VARIATIONS

1. MONOPOLY

One company is the only supplier in an industry, so it can set availability and prices as it wants.

2. PURE/PERFECT COMPETITION

There are many suppliers competing for customers, theoretically reducing prices.

3. MONOPOLISTIC COMPETITION

A small number of companies compete for customers.

4. MIXED

Some combination of the above exists. This is the system we have in the U.S.

4. SUPPLY & DEMAND

Supply is the number of units producers are willing and able to sell. Demand is the number of units consumers are

willing and able to buy. The point where supply meets demand is called the equilibrium price.

CHANGES IN DEMAND OR SUPPLY WILL AFFECT PRICES

A. If demand is constant and supply goes up, prices will fall.

B. If demand is constant and supply goes down, prices will rise.

C. If supply is constant and demand goes up, prices will rise.

D. If supply is constant and demand goes down, prices will fall.

5. BUSINESS CYCLE

An economy goes through natural cycles of expansion and contraction.

A. PROSPERITY

Times are good. Unemployment is low. Consumer spending is relatively high.

B. RECESSION

The economy is slowing down. Unemployment is increasing. Consumer spending is slowing.

C. DEPRESSION

The economy is weak. Unemployment is high. Wages are low. Consumer confidence is low. There is reduced

business activity.

D. RECOVERY

Business activity is picking up. Unemployment is going down. Wages are increasing. Consumers increase

their buying.

6. INFLATION & DEFLATION

Inflation is when the cost of items increase over time, thus decreasing the value of each dollar earned. Deflation is when the cost of items decrease over time, thus increasing the value of each dollar earned.

7. CIRCULAR FLOW

This is a diagram to illustrate how money circulates in our economy.

A. PLAYERS

I. HOUSEHOLDS/PEOPLE

II. BUSINESSES/ENTREPRENEURS

B. MARKETS

I. FACTOR MARKET

1. FACTORS OF PRODUCTION: NATURAL RESOURCES, LABOR, CAPITAL, & ENTREPRENEURSHIP

Natural resources are things like mineral ore, forests, water, or corn. Labor refers to the workforce.

Capital is investment in businesses through the buying of stock. Entrepreneurship is the

development of business ventures.

2. INCOME: WAGES, RENTS, INTERESTS, PROFIT

II. PRODUCT MARKET

1. FINISHED GOODS & SERVICES

2. PAYMENT FOR GOODS & SERVICES

The circular flow diagram can also be expanded to include the banking and government players.

8. IMPORTANT ECONOMIC INDICATORS

A. CONSUMER PRICE INDEX

This measures the cost to consumers of a hypothetical "basket of goods".

B. GROSS NATIONAL PRODUCT (GNP)

This represents the total value of all goods and services produced by a country.

C. UNEMPLOYMENT RATE

This generally represents the percentage of people who are both able and looking to work but cannot find a

job.

D. INFLATION RATE

This is the yearly rate of in the cost of things.

E. HOUSING STARTS

A good measure of how the economy is doing is the number of new houses constructed. This is because it

represents new and large investment, which is a good

indicator of both business activity and consumer confidence in future economic activity.